If you are building your path into venture capital — as an angel, scout, emerging fund manager, or operator transitioning into investing — 2025 offers something more valuable than momentum. It offers clarity.

According to the Canadian Venture Capital Market Overview 2025, the market closed with $8B invested across 571 deals. At first glance, that might look like a slowdown: deal count declined 12% year over year. But capital deployed declined only 6%, and average deal size rose to $14.07M — above the five-year average.

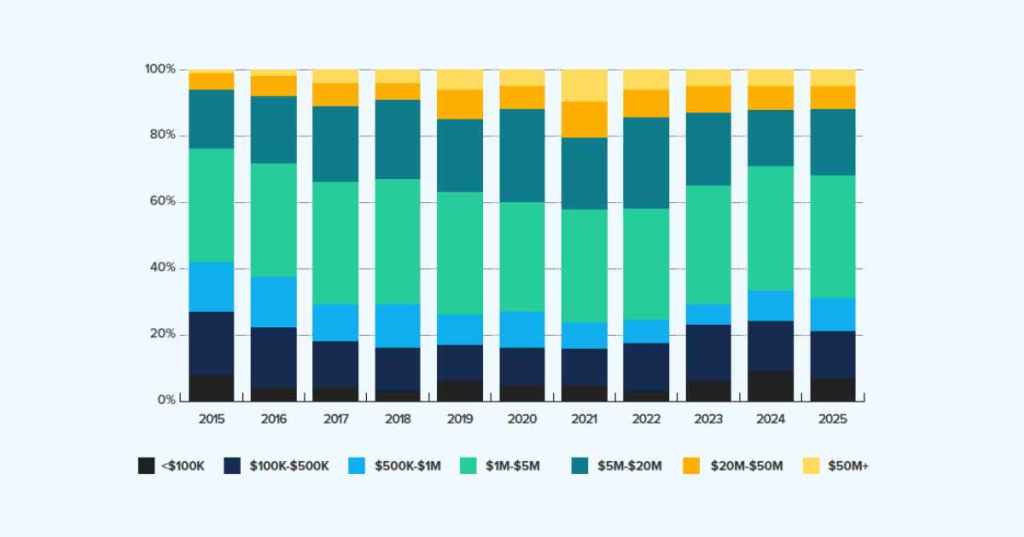

Over the past two years, capital has increasingly clustered around conviction. In 2025, just 26 mega-deals ($50M+) accounted for $5.3B — roughly two-thirds of total venture dollars deployed. Meanwhile, 88% of all disclosed deals were under $20M. The majority of companies are still raising capital, but the largest pools of capital are flowing toward companies that have already reduced risk and demonstrated measurable traction.

For emerging investors, this changes portfolio math. Entry price, ownership strategy, and reserve discipline matter more when capital concentrates at the top. In these cycles, the power law does not weaken — it intensifies.

This dynamic becomes even clearer when looking at stage allocation. Later-stage investment reached $2.7B in 2025, rising 25% year over year. Growth-stage capital increased 60%. Investors are not retreating; they are doubling down on companies with stronger signal quality.

If you are investing at pre-seed or seed, this raises important strategic questions. Do you have the reserves to support breakout performers? Are you building relationships with later-stage funds early? Are you underwriting with the expectation that follow-on capital will be more selective?

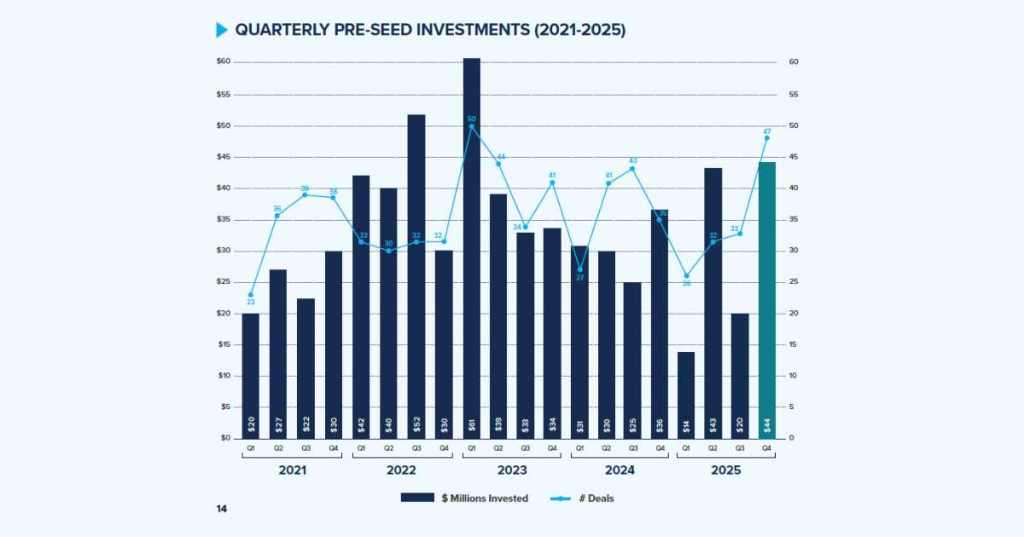

At the earliest stages, the picture is disciplined but stable. Pre-seed activity totaled $121M across 138 deals, representing 24% of all deal activity. However, the average pre-seed deal size fell to $0.88M — 15% below the five-year average. Capital is still flowing to early innovation, but underwriting standards are clearly tightening.

For emerging VCs, this is a test of rigor. Founder quality, early validation, governance readiness, and syndicate strength now carry more weight than vision alone. “Founder friendly” in 2025 does not mean unstructured — it means aligned and prepared.

Sector allocation also tells a story of concentration. ICT absorbed 64% of total venture capital invested in Canada in 2025, reaching $5.1B. Meanwhile, Life Sciences capital declined 47% year over year, and Cleantech declined 43%. Agribusiness, interestingly, rebounded sharply with a 78% increase in dollars invested.

These numbers are not instructions to chase momentum. They are signals of capital crowding and sector repricing. For disciplined investors, opportunity often lives where attention has temporarily cooled but fundamentals remain intact.

Another notable shift in 2025 was the decline in foreign participation. U.S. investor involvement dropped from 32% of deals in 2024 to 25% in 2025 — the lowest level of U.S. participation in Canadian mega-deals since 2016. That reduction in cross-border competition creates space. It can mean better pricing discipline and stronger domestic syndicates. For emerging Canadian investors, that is not a weakness in the market — it is a positioning opportunity.

At the same time, venture debt reached record levels, with $1.4B deployed across 69 transactions. Founders are increasingly building capital stacks that blend equity and non-dilutive financing. For investors, this adds complexity. Debt affects runway, risk exposure, and exit distributions. Understanding capital structure is no longer optional.

Taken together, 2025 reflects a venture ecosystem that is less euphoric and more analytical. It rewards underwriting discipline, reserve strategy, syndicate construction, and long-term portfolio design.

For emerging VCs, this may be one of the healthiest environments in a decade to build from. There is less noise. Less velocity for velocity’s sake. More emphasis on fundamentals.

In many ways, 2025 feels less like a contraction and more like a strategic reset.

And for disciplined investors, resets are where durable careers are built.

If you’re building your path as an investor and want a deeper understanding of venture funding dynamics, capital allocation, and portfolio strategy, we invite you to join our upcoming training sessions.

Learn how venture works — beyond the headlines.

Register to participate.

Leave a comment